2025 was supposed to be the year when container capacity through a continued injection of newly built vessel capacity was going to outstrip container demand, thereby taking pressure off freight costs.

In reality due to a number of reasons this has not happened.

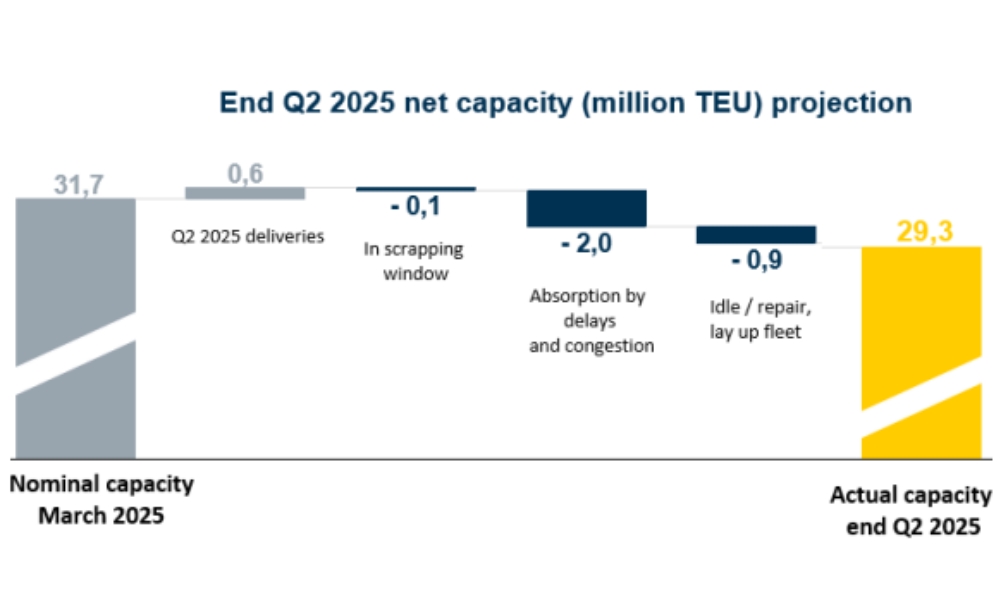

Whilst global TEU capacity started 31.7 million TEU in March, and new build vessel capacity for Q2 represents an injection of 600,000 TEU, this gain continues to be more than absorbed and offset by:

- Scrapping of outdated vessels (100,000 TEUs)

- Absorption by delays (e.g. Suez Canal Diversions) and Port Congestion (particularly through North Europe and USA) (2 million TEUs)

- Absorption by vessels idled / laid up / being repaired (900,000 TEUS)

This has led to a net reduction in global capacity by end Q2, with pressure remaining on freight markets across the globe.

These uncertainties and imbalances are expected to continue to end 2025, with:

- No end in sight to diversions of the Suez Canal

- Continued uncertainty surrounding the impact of tariff policy in the US and impact on trade flows globally

- Potential impact of US Government imposed special taxes on Chinese built vessels calling at US port (from October 2025)

- Congestion in North Europe showing no signs of abating

Specifically in Australia, we see no major or new injection of extra capacity, so similarly we see volatility in local freight markets continuing. This all points to ongoing volatility on service levels and freight markets.

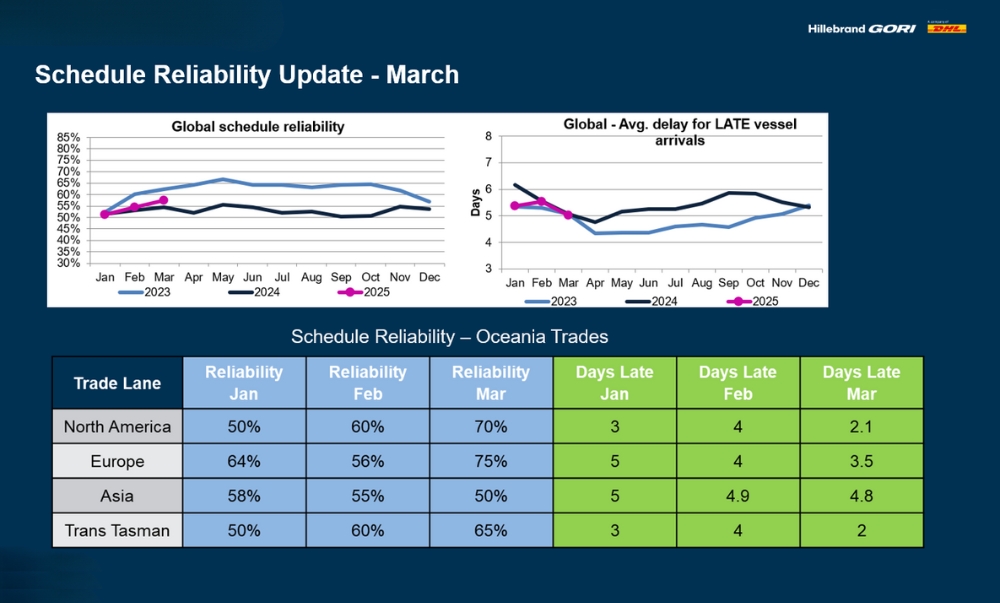

Schedule reliability because of the ongoing congestion also remains challenged, particularly in Oceania.

Hillebrand Gori, via their extended global network and key freight shipping line contracts and options, can help in navigate these volatilities. Stay updated on shipping trends or learn more about Hillebrand Gori.