Liquor purchasing has become omnichannel. Consumers now flow across traditional On Premise, Off Premise retail, digital platforms, and experience-led spaces more seamlessly than ever.

This creates huge opportunity but also intense fragmentation for suppliers trying to understand where their category is winning or losing, and critically, where to invest next.

For brands, the challenge is not to “be everywhere” but rather it is about showing up in the right places to meet the needs and motivations of their current and target consumers.

Winning in today’s landscape requires:

- continuously tracking where consumers are buying, drinking and consuming

- understanding how channels compete, complement, and reinforce each other

- developing a channel strategy that adapts as occasions shift

The consumer evidence behind this is compelling:

- 60% of Australians say they repurchase brands they try in On Premise venues when later shopping in retail stores.

- 43% say they have purchased a drink in retail or On Premise directly because they saw it on social media/online.

Discovery, trial, and replenishment are now interconnected — and channel strategy must reflect this.

Retail remains the cornerstone but faces continued pressure

Retail still anchors the liquor category, but engagement is softening.

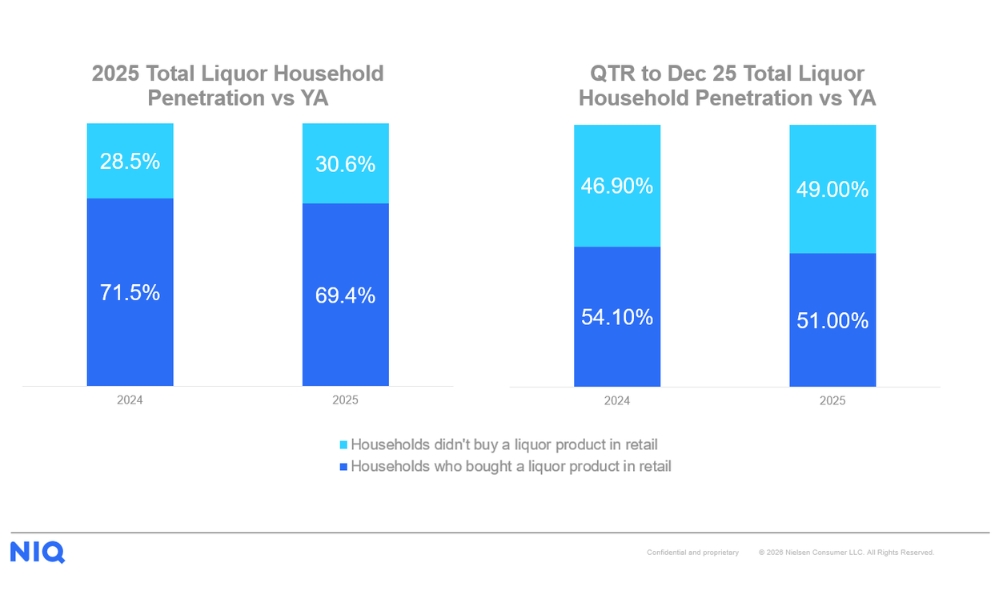

- 69.4% of households purchased alcohol at least from retail stores across the whole of 2025, down from 71.5% in 2024.

- In the most recent 12 weeks, this dropped again to 51.0%, down from 54.1% the same period a year earlier.

- Purchase frequency is also down 4.9%, though higher spend per occasion has softened the blow.

With fewer shoppers entering the channel and those who do buying less often, the traditional volume engine for liquor is under structural pressure. Brands relying solely on Off Premise retail risk future share loss unless they activate new touchpoints.

On Premise sees contrasting fortunes

The On Premise continues to be a barometer for category health, but performance is diverging sharply.

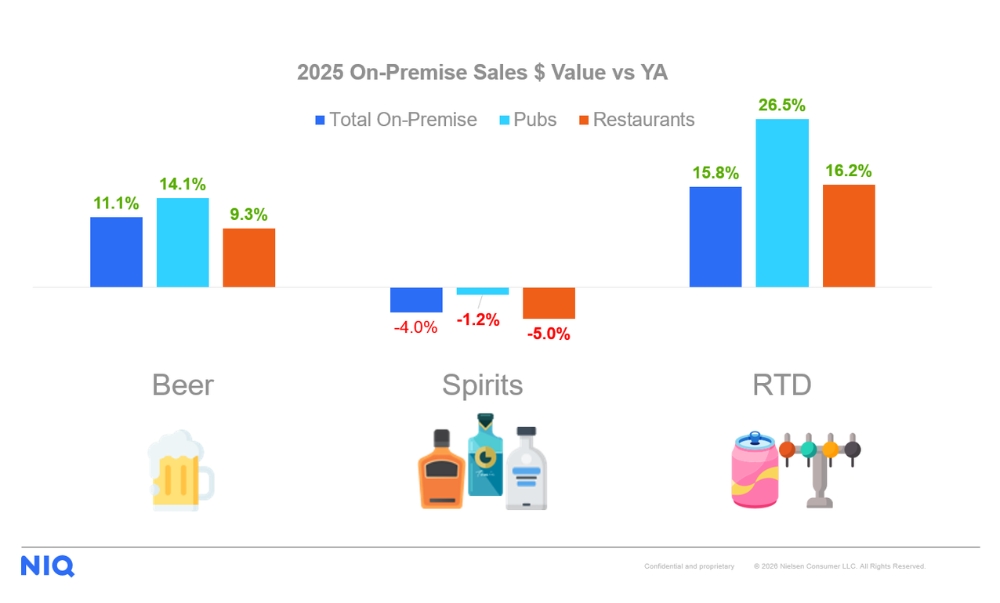

- Beer has delivered strong value growth, up +11.1% YoY.

- Glass spirits have declined -4.0% YoY.

- RTDs delivered the fastest growth rate, up +15.8% YoY.

Subchannel breakdown shows pubs as the standout performer for all categories:

- Beer in pubs: +14.1% vs +9.3% in restaurants

- Spirits in pubs: -1.2% vs -5.0% in restaurants

- RTDs in pubs: +26.5% vs +16.2% in restaurants

However, value perceptions remain a universal challenge. When ranking visit attributes by satisfaction, “overall value for money” scores lowest, and consumers rate spirits, cocktails, and RTDs as the least satisfying categories on value.

What this means:

- Beer must continue leveraging momentum through value cues and sessionable occasions.

- Spirits need to re-earn value perceptions through elevated serves, mixology, price clarity, and experience-led premiumisation.

- Despite value for money perceptions, some RTDs are clearly winning this battle, with draught in particular driving the growth of RTDs.

Online retail grows strongly off a small base

Digital continues its surge, albeit from a smaller starting point.

- E-commerce liquor sales through bottle shop websites grew +16.2% in the last year.

- The number of shoppers buying liquor online increased +14.1%.

Yet the headroom is striking:

- Only 8.3% of households purchased liquor online in the last year.

- In comparison, 24% of households bought non-liquor products online from Woolworths and Coles.

And online is disproportionately valuable:

- The average online liquor basket is 2.4× higher than an in-store basket.

Cracking the online code is a major growth unlock, especially for gift-giving, planned occasions, event hosting, ultra-convenience and premium shoppers.

Experience-led channels offer a powerful brand-building platform

As consumers increasingly seek more than just a drink, experience-led On Premise venues are quickly becoming high-impact brand discovery hubs.

In Australia:

- 14% of consumers attend festivals

- 13% visit stadiums

- 10% visit arenas

- 10% visit game-based experience bars

These channels aren't peripheral. They are recruitment engines that enable brands to leverage partnerships, sampling, rituals, and immersive activations.

Consumers choose these venues because they offer:

- Something fun (49%)

- An engaging activity with friends or family (41%)

- Interactive entertainment (34%)

- An exciting experience (34%)

This reinforces a crucial point: people are not going out for a drink. They are going out for an experience.

For brands, this means activations must enhance the look, feel, and energy of the venue, not sit alongside it. The brands that win here create experiences that consumers take with them into retail, online, and everyday drinking occasions.

So what? A clear call to action for brands

The consumer journey is now non-linear. A brand discovered in an arena may be bought online, reposted on social media, gifted to a friend, and replenished from a bottle shop.

To win in this omnichannel world, brands must:

1. Map their consumer’s channel journey, not just their purchase point

Where do discovery, trial and repeat actually happen?

2. Invest in the channels that shape behaviour, not only those that capture volume

Experience-led venues and digital frequently drive first or premium interactions.

3. Break down channel silos internally

Brand, category and digital teams should work from the same omnichannel plan, not separate ones.

4. Make On Premise and Online work harder as discovery engines

These channels disproportionately influence retail sales.

5. Measure what matters

Penetration, cross-channel conversion, and frequency are now more telling than pure sales.

The brands that thrive will be those that treat every channel as part of a connected system, not a standalone battleground.

Industry momentum: A new thought-leadership program begins

To help the industry stay ahead of these shifts, we are launching a new insight sharing thought leadership calendar partnership between NIQ and the Drinks Association. The first theme in this series focuses on omnichannel behaviour and its growing influence on discovery, trial and purchase. Throughout the theme period, we will release targeted insights and practical frameworks, culminating in a live webinar that brings the industry together to unpack the findings and explore how to activate omnichannel strategies with confidence.

Register to attend the first webinar, "Understanding the new omnichannel landscape."

NIQ is a Platinum Partner of the Drinks Association.