Small business struggling as late payments take hold

The October 2022 CreditorWatch Business Risk Index (BRI) has revealed that small businesses are feeling the pinch of the current economic pressures while big business is faring much better.

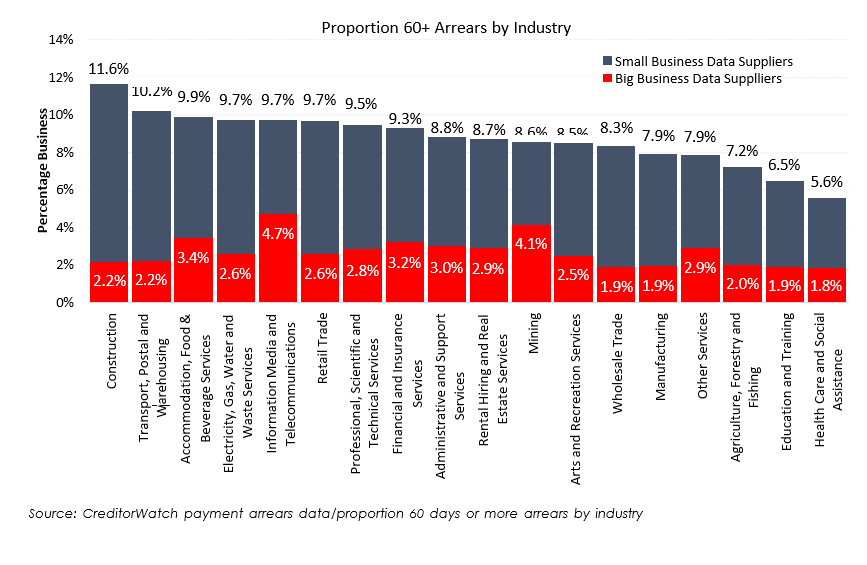

Across all industries, late payment rates for small businesses are averaging three times that of big business, reflecting the challenge small business faces enforcing payment terms and collecting on payment arrears.

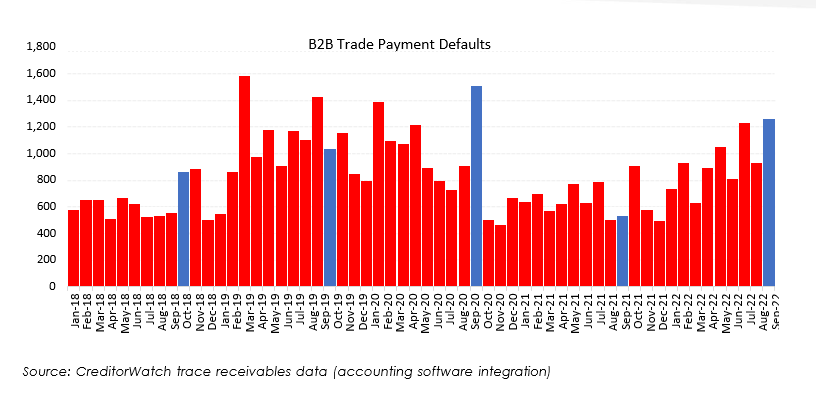

Trade receivables for small business have dropped 18 per cent in the past month, to the lowest levels since October last year, while payment defaults have continued to increase at a rate of 20 per cent per month over the past year.

In contrast big business has not suffered the same decline in trade turnover. Revenue in big business is up 14 per cent from FY21 to FY22 across all public companies and ASIC reporting entities. Profits are up nine per cent despite reduced margins.

Key Business Risk Index insights for October:

• YoY growth in B2B trade receivables is flat, pointing to a softening in recent small business trade activity recovery

• B2B payment defaults have continued to increase at an average rate of 20 per cent per month over the past year

• Late payment rates are on average three times greater for small business relative to big business

• Revenue across big business is up 14 per cent from FY21 to FY22 across all public companies and ASIC reporting entities. Profits are up nine per cent despite reduced margins.

• Big business profit margins are down slightly as a result of increased operational expenses. It is expected that margins will be compressed further in FY23 as the full impacts of inflation are realised

• External administrations have dropped by 34 per cent since September

• Court actions have decreased 26 per cent since last month but are still up 50 per cent year-on-year

• Yarra Ranges in Victoria is the region with the lowest insolvency risk (across regions with more than 5,000 businesses), followed by Cottesloe-Claremont in Western Australia

• The Western Sydney regions of Merrylands–Guildford and Canterbury are the regions at highest risk of default across Australia (for regions with more than 5,000 businesses)

Trade Payments to Big vs Small Business

CreditorWatch CEO Patrick Coghlan says a lack of capacity to collect payments is starting to have a serious impact on small business trade.

“Our Business Risk Index data highlights that small business’s limited capacity to enforce payment terms and collect payment arrears is having a significant impact. Trade receivables continue to decline and trade payments defaults, a lead indicator of insolvencies, are at their highest point since October 2020. Small businesses are crying out for additional support which is one of the reasons why earlier this month we launched CreditorWatch Collect - an automated receivables management software and collections service provider. We want to help businesses get paid faster.”

According to CreditorWatch Chief Economist Anneke Thompson, nearly all of the important forward looking indicators - consumer & business confidence, job vacancies and B2B trade defaults - are showing clear signs of deterioration.

“Instinctively, this seems unwanted, but unfortunately a significant slowdown of the economy is one of the only cures for inflation,” she says. “The challenge is not allowing small business to suffer the brunt of the impact of a slowing economy, which unfortunately is usually the case.

“Small businesses need to exercise extreme financial discipline, and we are already seeing signs of this in increasing B2B trade defaults, as this means businesses are taking action when they are not getting paid. Over the next year to two years, cash flow will be king, and small businesses should be as ruthless as big business in demanding invoices owed, and using all resources available.”

Probability of default by region

The five regions* at least risk of default over the next 12 months are:

1. Yarra Ranges (VIC): 4.81 per cent

2. Cottesloe-Claremont (WA): 4.92 per cent

3. Adelaide City (SA): 4.95 per cent

4. Ku-ring-gai (NSW): 5.01 per cent

5. Geelong (VIC): 5.01 per cent

The five regions* most at risk of default over the next 12 months are:

1. Merrylands-Guildford (NSW): 7.79 per cent

2. Canterbury (NSW): 7.55 per cent

3. Auburn (NSW): 7.44 per cent

4. Surfers Paradise (NSW): 7.42 per cent

5. Ormeau-Oxenford (QLD): 7.38 per cent

* Regions with more than 5,000 registered businesses

Once again, areas with high levels of personal insolvency are most exposed to business insolvency. We expect this to be a continuing trend, as personal and business finances tend to blur in times of high financial pressure.

Probability of default by industry

The industries with the highest probability of default over the next 12 months are:

1. Food and Beverage Services: 7.2 per cent

2. Arts and Recreation Services: 4.6 per cent

3. Transport, Postal and Warehousing: 4.6 per cent

The industries with the lowest probability of default over the next 12 months are:

1. Health Care and Social Assistance: 3.2 per cent

2. Agriculture, Forestry and Fishing: 3.5 per cent

3. Manufacturing: 3.6 per cent

The discretionary spending sector is already starting to slow down, even if this is difficult to see via Retail Trade data, as dollar volumes are now likely increasing as a result of inflation. The big spending Christmas period will be very telling for many businesses, and likely set the scene for what 2023 has in store.

Spending over Christmas 2021 was heavily impacted by large amounts of savings consumers had to spend, as well as the 'revenge spending' phenomenon. Now, consumers have a whole different set of challenges to think about - most of them leading them down the path of spending less.

Outlook

As outlined by the Treasurer in the October 2022 Budget update, the outlook for the economy in 2023 is quickly deteriorating. There is no doubt conditions will be more challenging for Australian businesses In 2023. Much of the impact, however, will depend on how deeply the severe monetary policy tightening in the USA, UK and Europe hits those economies. While recession is still unlikely in Australia, the same cannot be said for those economies, and that will have real consequences for Australian businesses in 2023.

Register here to receive Creditorwatch's Business Risk Index updates as they are announced.

Creditorwatch is an Associate Member of the Drinks Association.